I’d like to say I’m a casual “travel hacker,” but truthfully, my family’s travel adventures depend heavily on strategic credit card use. I’ve had the travel bug since my first trip to Italy at the ripe ol’ age of seventeen, armed only with a student Visa card with a $500 limit (most of which went straight into a leather jacket in Florence—a questionable choice at the time, but hey, I still have it, and it still looks good!).

Back then, credit cards were simply safer and easier to replace than traveler’s checks or debit cards—something I firmly believe still holds true today. Over the past fifteen years or so, I’ve significantly upped my game, discovering how smart use of credit cards can literally transform travel from something we dreamed about to something our family does regularly.

Important note: Responsible credit card use is essential. I only spend what’s already in our budget, treating credit cards as if they’re debit cards. Paying interest defeats the purpose, so be careful and strategic!

View this post on Instagram

I still have a lot to learn, but I definitely do you know how to use the loyalty programs and leverage sign on both bonuses to significantly reduce our travel costs.

This post is intended to be a guide to using credit cards to dramatically reduce travel costs for the beginning travel hacker.

What Exactly Is Travel Hacking?

When you use credit cards for travel hacking, you basically open credit cards, use referrals, shopping bonuses and sometimes (strategically) close them, in order to utilize large sign on bonuses and loyalty points to earn cheap travel.

Travel hackers…. or in my case just a travel frugalista….realize that passing up on the bonus offers and rewards that a travel credit card offers, in lieu of a debit card or cash, shortchanges you on the opportunity to travel like you want to…or to have more money in your wallet when you arrive . Failing to utilize credit cards to your advantage passes up a chance to earn discounts and possibly even free plane tickets, car rentals and hotels and experiences.

[bctt tweet=”Failing to utilize credit cards to your advantage passes up a chance to earn discounts and possibly even free plane tickets, car rentals and hotels and experiences.” username=”flipflopweekend”]

Now, this is where people get nervous.

Credit cards need to be used responsibly. You only save money for travel with them, if you don’t overspend.

Seems obvious. But, when you are using credit cards to get travel points, the goal is to save money…not spend more of it!

[bctt tweet=”When you are using credit cards to get travel points, the goal is to save money…not spend more of it! Click to read more” username=”flipflopweekend”]

Use the credit card as you would a debit card. Pay it off monthly and then you don’t accrue the high interest fees or late fees. It also does not hurt your credit that way…in fact, it can actually help.

Many credit cards offer very lucrative sign on bonuses and high-level rewards just for the honor of having you as their customer and it’s really to your benefit if you know how to work the system and travel to your chosen destination on a shoestring budget.

Where Do I Start and How Do I Know Which Card To Get?

If you have lived in any one place long enough you probably have received all of the ‘junk mail’ with different credit card offers and automatically thrown them away.

With all of the options, it’s tough to know which one to apply. Nowadays, credit cards are everywhere, relatively easy to obtain and we use them to pay for everything you can possibly pay for… from high ticket items like televisions and appliances all the way down to that $.79 soda at the gas station .

And deciding the best credit cards for points for travel is not a one size fits all approach. Several items we need to be taken into consideration as you consider which card to start with as a newbie ‘hacker.’

For example:

Are there certain airlines that you’re loyal to?

Are you willing to fly any carrier?

What are your spending habits?

Do you drive more often than fly and would rather use points towards hotels or car rentals?

Asking yourself these questions will help you determine the type a traveler you are and you’ll be well on your way to figure out the best card for you.

I have a Cash Back Card. It’s the Same Thing, right?

Many people already have a card that offers cash back rewards such as the Chase Freedom card or the Discover IT card. But, how do they stack up?

The obvious difference is that cash back cards can earn you cash back rewards, which can be utilized for any purchase. However, travel reward cards will limit your rewards to travel related expenses.

For this reason alone, the right card depends on your goals. I like to earn points specifically for travel…so I stick with travel cards or cards that have travel rewards. If you want more flexibility, a cash back card may be more ideal.

How Much Can I Earn When I Use a Credit Card For Travel Rewards And How Do I Redeem Travel Reward Points?

The typical redemption rate of rewards is 1:1

That means one reward point equals a penny. My husband is the math guy, but I know that basically would turn 10,000 points into $100…regardless of whether it’s travel points or cash back.

Now, there are cards which will earn a higher rate, especially airline credit cards. If you are loyal to one airline, this may make sense. Airline branded cards ( like the United Explorer card or Delta Skymiles) will offer extra perks like priority boarding, free baggage or more. These cards will require you to book directly through the airline or hotel portal.

However, if you are a more flexible traveler, then a bank travel card with more open ended options ( my preference) is the better way to go. These cards typically allow you to redeem rewards in the form of statement credits after you have made a travel purchase.

Travel Card Perks To Consider

When selecting the best Travel credit card for you, there are a couple of key components you will want to check.

- Sign On Bonus

When looking at the offers available to you for a travel credit card, the number one thing you want to be looking for is the sign on bonus.

You want to make sure that you are being offered a significant number of points for rewards to help you perhaps get a free plane ticket (or two) after making the minimum introductory spend within a defined timeframe.

50,000 – 60,000 bonus points is about the average amount of points for a typical card sign on bonus, but sometimes there can be special values where they can be higher.

Most cards I have used have a spending threshold of three months. Some of these spending thresholds could range from $2,000 to $5,000 within a two or three month period.

However, the Bank of America Travel Rewards Card has a smaller sign on bonus compared to others, but you only have to spend $1000 within the first couple of months to earn 25,000 points…worth $250 in travel rewards.

We made a $700 car repair (not fun) on this card, paid the card off right away from our sludge fund ( which you absolutely should have for those types of emergencies). After a couple more trips to the grocery store and gas station, we had about $250 worth of travel back in our pockets.

- Bonus categories

Often times cards will give you additional points if you make purchases within certain bonus categories.

Sometimes ,this could be a matter of just using the brand products of the credit card. For example, the Choice Hotels credit card will offer you a one point for every dollar spent. However, if you book a hotel with that card you can get 15 points for every dollar spent. So, if you are a frequent traveler or frequent family traveler who utilizes one of the Choice hotel chains, then the card could be very lucrative for you if you use the card to pay for those hotel rooms.

Other cards may offer bonus points for purchases related to travel including car rentals , gas, or for every day activities like eating out.

This is one of the reasons why I like my Chase Sapphire Preferred Card. The card is considered one of the gold standards when it comes to travel credit cards, especially for travelers who want more ‘oomph’ than a no-annual fee card (more on that in a moment), but don’t really travel enough to make a more premium card like the Chase Sapphire Reserve worth it.

With the Chase Sapphire Preferred, not only do I earn one point for all of my every day purchases like groceries, but I can earn two points per dollar on eating out. Plus, they have some ‘loose’ definitions on these categories, so even when we refill our popcorn bucket at Walt Disney World, it’s considered ‘eating out.’

You can also get double the points on travel, which ,again, is also very open ended. So, that category will include things like taxis, trains, and that Uber rental from your home to the airport.

Get your first ride Free on Uber when you sign up throughmy referral link or use the code keril946ui .

However, Chase has a strict 5/24 rule when it comes to opening new cards.

Basically, if you have opened five or more credit cards within the past 24 months. If you are close to limit and think you want a Sapphire card, snag it now so you are free to hack with other cards, as well, in the next two years.

- A manageable minimum spending threshold

There’s no point in signing up for a card that requires you to spend $50,000 in the first three months when you feasibly only spend $4,000 a month on household purchases or less.

That’s just going to force you to overspend and is financially irresponsible. When you start making purchases just to put more money on the card to get a sign on bonus, which means you can’t pay it off right away, you start accruing interest and potentially set yourself up for late fees.

Once again…only use credit cards for travel hacking purposes if you can pay off the credit card each month.

The only exception is if you plan on using the card for a major purchase and the card has 0% interest introductory rate that is long enough for you to pay off that card within that time frame. In those instances, divide the amount you owe, by the number of months in the introductory period and plan that amount in your monthly budget the same as you would a mortgage or car payment. Do this before you make the purchase!

Also, don’t open up several cards at a time with minimum spending thresholds. Focus on one at a time to start. Otherwise, you will stretch yourself thin and find it a bit difficult to manage.

- Foreign transaction fees

If you typically stay domestic in United States, then this isn’t that big of an issue.

![]()

However if you are aiming to fly to an international country (or drive… cheers to you, Canada and Mexico), then you are going to have to pay attention the fact that a lot of credit cards will charge an additional 3% or better for the mere privilege of using your credit card in another country. This is above and beyond any currency conversions fees that may also be included. SmartAsset has a great post to help you understand the difference between foreign transaction fees and currency conversion fees.

Fortunately, there are a lot of solid travel credit cards out there that waive this foreign transaction fee. However, there are some that don’t so it’s definitely something to check when you are a listing potential cards to apply for.

IMPORTANT TRAVEL TIP:Foreign transaction fees can be avoided with a card that waives them. Currency conversion fees may not be, but they can be minimized. If you make a purchase overseas with your card, always choose “local currency.” If you choose for the merchant to convert to U.S. Currency, they will more than likely factor in their own rate for the conversion…and it will be much higher than what your bank or credit card would charge. If you really need to know how much you are actually spending, download a travel app currency conversion calculator.

Annual Fee or No Annual Fee — That Is The Question…

If you are dabbling in credit card travel hacking and looking for a simple card to sign up for, I would suggest starting with a no-annual fee card. Annual fee cards oftentimes do have higher reward rates, but can cost you if you don’t use them enough to get a higher return in value.

I just recently went with the Chase Sapphire Preferred card, which has a $95 annual fee, because I determined that my spending on the card and the reward return, would ultimately net me more reward money than the cost of the card. Plus, the annual fee is waived the first year which will give me some time to use the card and see if my estimations were correct. Update as of June 2019: The annual fee is not waived, however the bonus has increased by 10,000 points… which is basically the value of the annual fee.

Many reward credit card applications will have some type of calculator to help you estimate your ROI (return on investment) of a particular card. Nerdwallet.com has some amazing calculators and card comparison functions to help you make this determination.

What Does Travel Hacking Credit Cards Do To My Credit Score?

This is probably the first question that popped into your mind.

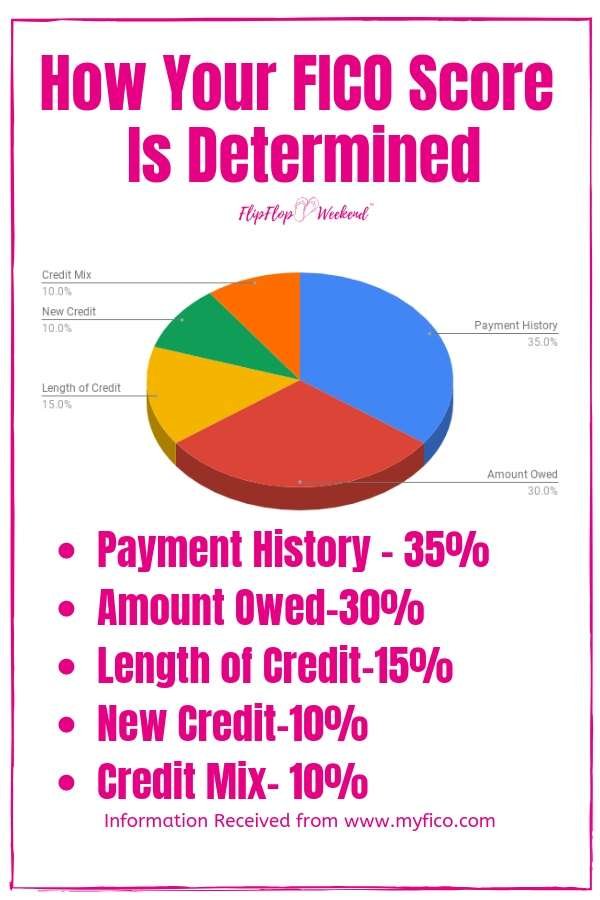

Let’s take a look at how credit scores are determined:

The technical term for your credit score is your FICO score. This score is the basic measurement that will be used to assess your ability to pay back a lender for loans…such as student loans, mortgages, car payments and….credit cards. Lenders want to make sure that you are not a risk for them.

Your FICO score is the result of a data analysis on a few key components in your financial profile:

- Payment History–

- The most important factor in your credit score is whether or not you make on-time payments to your accounts.

- Amount owed-

- This doesn’t necessarily mean the total amount you owe…but it does mean your debt to credit ratio. For example, if you have $10,000 worth of credit extended to you, and you have $9,995 worth of debt on that card…then other lenders may see you as high-risk or overextended. However, if you have $100,000 worth of credit available, and only $2,000 utilized, your debt to income ratio is much lower. This is why having several cards, even with zero balance and paying off used cards monthly, can actually boost your credit score.

- This also means that you generally want to avoid closing cards. Unless there is an annual fee and the card will be unused, try to keep your accounts open…even if that means making a small $5 purchase on each one here and there.

- Length of Credit –

- How far back does your credit history go? Newer borrowers will likely have to start with smaller, more low risk cards as they build a credit history. Borrowers with longer, more established histories are oftentimes given better offers.

- New Credit-

- How many cards or loans have you opened recently? Try not to open too many cards at one time…especially before making a major purchase like a house or car. With every credit application, you will see a small ding to your credit. Since this is a small percentage of your overall score, it’s usually only a couple of points and goes away after a couple of months. For this reason, though, leave some time between applying for and opening cards.

- Credit Mix-

- How is your credit varied? Is all of your credit in the form of credit cards? Or is your overall credit profile made up of credit cards, mortgage, car payment, student loan, etc? This is a small part of your loan and in no way am I saying you should have all of these. By all means… try to get out from under your student loan debt and car payments. But, it is worth noting that this information is looked at in determining your score.

Your FICO score is analyzed and reported by three major companies…TransUnion, Experian and Equifax. It can be costly and time consuming to check your score with all of them, which is why I like to use CreditKarma.com

Credit Karma is a free and secure credit monitoring site where you can check your score for fluctuations. They will also notify you if they see something amiss. I have been using it for years and definitely recommend it.

The bottom line, however, is that you can still open and have multiple credit cards and still have a good score.

This is my actual credit score as disclosed by Credit Karma and I have nineteen credit cards reported on my account. Most of those, however, have no balance, the others are paid monthly and my oldest account currently on record is from 2009.

Finally…Some Recommendations!

First, check your credit score either on CreditKarma or by getting a copy of your free annual credit report. Then, check out some of these top credit card picks based on my research of reviews online and also the cards I have in my own wallet.

Travel Credit Cards for Bad Credit (Between 300-579):

My actual recommendation here is to build your credit before applying for a rewards card. Your options will be limited.

Perhaps consider a store credit card for some place that you typically shop ( ie. Target RedCard) as a starting point. Remember, just make small purchases on the card that you can pay off right away…otherwise, your credit will get worse.

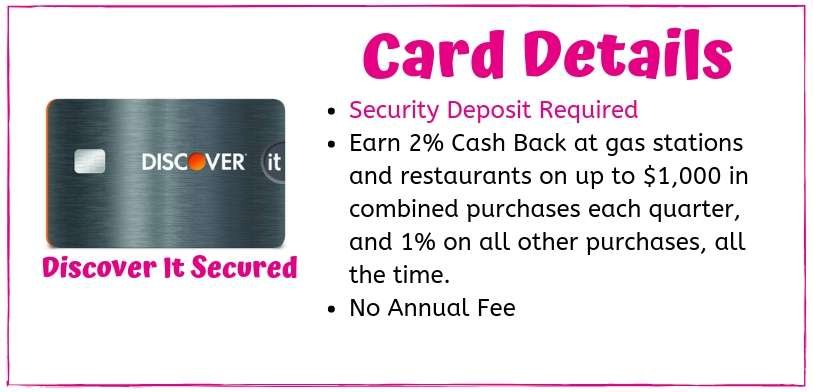

However, if you really want to get a standard rewards card, you can look into a secured card.

The Discover IT Secured Card. This is not a travel reward card, but a cash back card that can get you headed in the right direction.

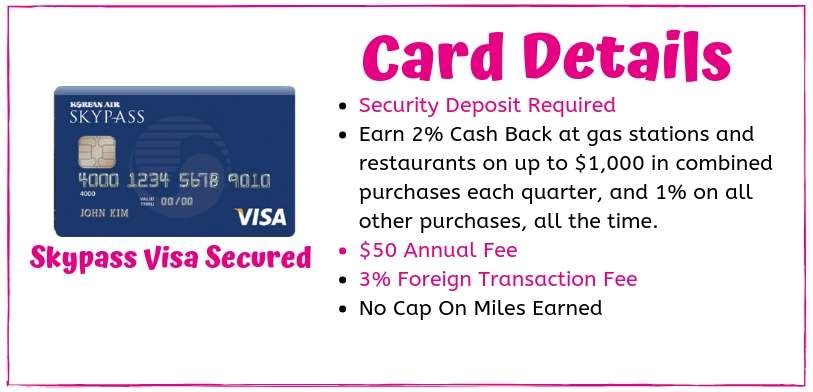

For those with a rough credit history, the Skypass Visa card has the benefits of being able to earn miles even with bad credit. Plus, the card is more flexible than a Discover since it has better accepted worldwide due to it being a Visa card. However, you do need to weigh the pros against the cons of it having an annual fee and the foreign transaction fee.

Travel Credit Cards for Fair Credit (580-669):

This is a tough range and, again, my recommendation is to try to get your score above a 670 for the magic starts to really happen. For information purposes, you can look into the CreditOne Platinum Visa card since it does offer a cash back option. However, the high annual fee makes it a risky option and I think you could do slightly better with one of the secured cards mentioned above if you are trying to build your credit.

If you are on the higher end of the Fair Credit range, you may get lucky and get approved with the CapitalOne Venture One card, which I mention in the next section.

Travel Credit Cards for Good To Excellent Credit (670-850):

Click here to learn more about the CapitalOne Venture One Card.

Credit Cards for Traveling Students

And to bring it back full circle… here are some picks for students who want to travel (just in case they want their own leather jacket), but need to build their credit.

Student credit cards tend to have higher interest rates… so, if you are a student, make sure you are educated about debt management and only put expenses that you can pay off monthly. Which means….don’t go buying pizza for everyone in your dorm… unless of course, you can actually afford it. In that case, you’re so generous and I bet they like pepperoni.

Do you currently utilize a credit card for travel rewards? I would love to know which one is your favorite. If you still have questions about how to utilize travel credit cards for discounts, please let me know in the comments so that I can add to this post and help you out! Bon Voyage!

Kelly

Thank you for posting this! I just signed up for a southwest Visa because I won a competition at work and the prize was a southwest gift card. They have a ton of options on their website for flight, hotel, and car rental. Their rewards program is spending $4000 in 3 mo months gets you a travers pass (a FREE) plane ticket for the rest of the year and it’s only February! I’m super excited about it!

Keri

Awesome! What a great prize! The Southwest Rapid Rewards card is a nice card with a lot of options. I don’t have a lot of experience with it yet, because I wanted to grab my Chase card but I am sure I will try it out in the future. I know a lot of fellow travel bloggers have great things to say about it. Where do you plan on going with your prize?

Taryn

This is such a great comprehensive post! I’m going to book mark it. We plan on moving next year and I’d like to utilize a rewards card like this (even though we will have the money saved) to collect some points on that as well. Thanks for sharing these tips!